.svg)

.svg)

Download Brouchure

%202.svg)

Oops! Something went wrong while submitting the form.

Raw material price forecasting is a mission-critical function that directly determines profitability in the construction and manufacturing industries. Since 2025, the global commodities market has exhibited unprecedented levels of price volatility as geopolitical conflicts, trade tariff overhauls, and energy price surges converge simultaneously. In an environment where core materials—iron ore, copper cathode, nickel, and rebar—swing 10% to 30% within a single quarter, legacy experience-based sourcing and simple statistical models are proving insufficient for timing procurement decisions accurately. This article examines the true nature of raw material price risk confronting the steel and construction sectors, and provides a step-by-step guide to how AI-powered forecasting technology can support procurement decision-making.

Raw material procurement in the steel and construction industries presents a particularly high degree of forecasting difficulty compared to other sectors. The reasons lie in several characteristics unique to these industries.

Raw materials in the steel and construction industries are priced not by any single factor but by the intersection of multiple macroeconomic variables. Iron ore prices are influenced by China's domestic steel production volumes and global greenfield mining project pipelines. Copper cathode prices are linked to international crude oil prices and electricity grid demand from AI data centers. Nickel supply fluctuates significantly depending on the Indonesian government's production quota policies. And rebar prices can diverge dramatically by region in response to U.S. trade tariff policies.

In practice, these compounding variables operated in concert during the period from 2025 through mid-2026, producing severe impacts on individual commodity prices. In the case of nickel, Indonesia's aggressive production expansion pushed the 2025 London Metal Exchange (LME) average price below $15,000 per tonne. However, when the Indonesian government tightened environmental enforcement in early 2026 and sharply reduced production quotas, prices staged a dramatic reversal—rebounding nearly 30% within a single month. Copper cathode surpassed $14,500 per tonne in January 2026, reaching a historic high, before retreating to the $13,500 range in Q2 amid U.S. Federal Reserve tightening concerns—oscillating in $1,000-per-tonne swings.

One of the most complex challenges procurement teams faced in H1 2026 was the phenomenon of the same commodity moving in entirely opposite price directions depending on the region. After the U.S. government overhauled Section 232 metal tariffs, imposing tariffs of up to 50% on imported steel and semi-finished copper products, domestic U.S. rebar prices rose more than 7% quarter-over-quarter to $1,015 per tonne in Q1 2026. Meanwhile, Asian and European steel volumes—now locked out of the U.S. market—flooded into non-sanctioned regions, pushing rebar prices in Taiwan down 17% over the same period to $585 per tonne.

In an environment where a single policy change produces diametrically opposite price movements across regions, procurement decisions cannot be based on historical averages or trends from any single market alone. Geographic diversification of supply sources, combined with the ability to precisely identify price drivers in each regional market, is becoming a core element of procurement competitiveness.

Separate from short-term volatility, structural forces are also exerting upward long-term pressure on raw material prices. Copper demand is growing rapidly as AI data center construction and power infrastructure expansion accelerate worldwide. According to Gartner, global data center electricity consumption is projected to increase 26.4%, from 447 TWh in 2025 to 565 TWh in 2026. The resulting expansion of transmission and distribution infrastructure is a persistent driver of copper demand. High-purity nickel used in EV batteries is also expected to see growing long-term demand, and some forecasts suggest that once the current supply glut subsides, the market could actually shift into deficit by 2028.

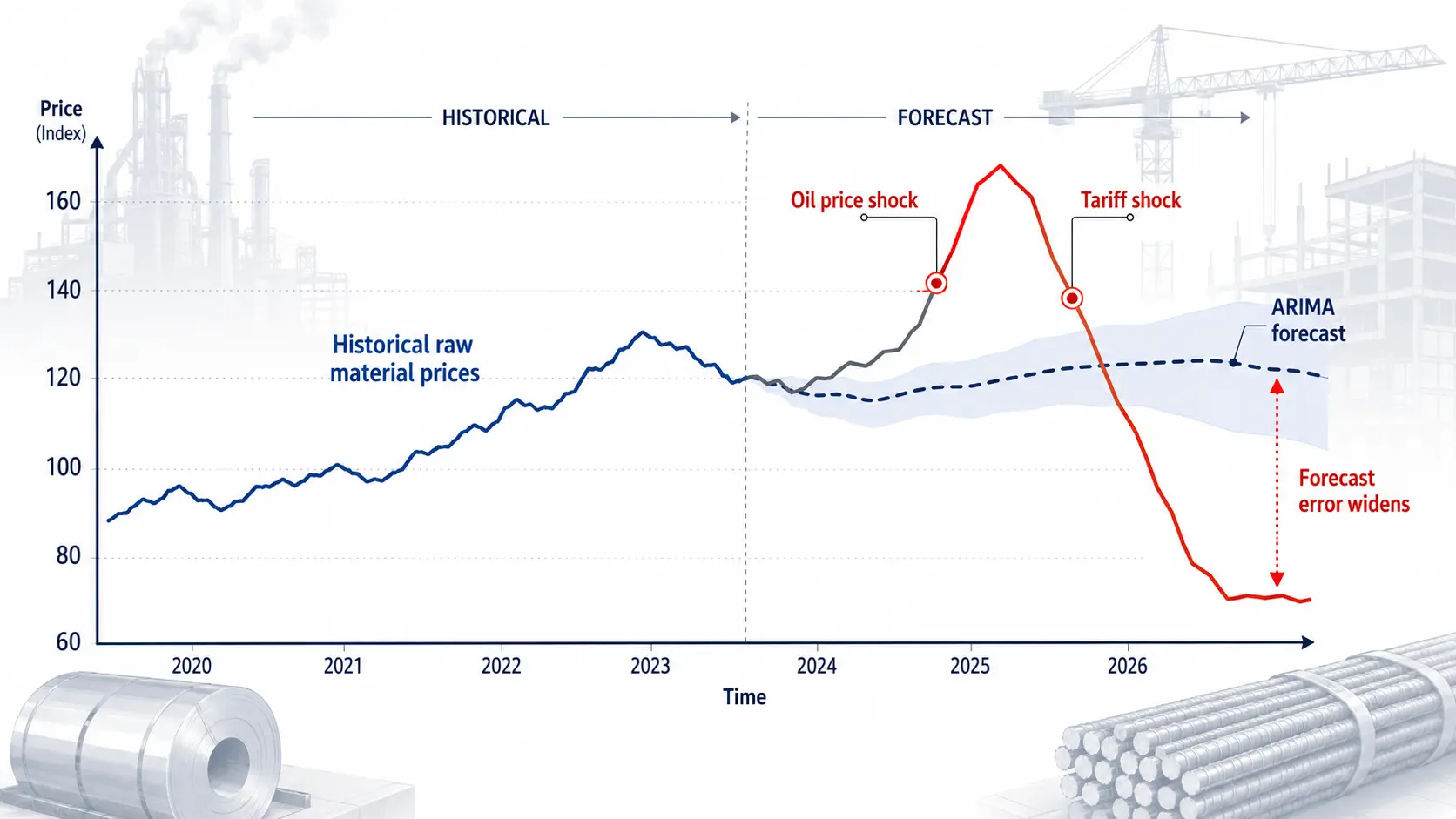

The most common method that steel and construction companies have used for raw material price forecasting is time-series statistical models such as ARIMA (AutoRegressive Integrated Moving Average). In simple terms, ARIMA tracks patterns in historical prices to estimate the direction of future prices, and it can serve as a useful reference when prices follow a relatively stable trajectory.

However, this approach has several structural limitations. First, ARIMA operates on the assumption that the mean and variance of the data do not change significantly over time. Sudden shocks—such as a Strait of Hormuz crisis or the imposition of large-scale tariffs—violate this assumption, causing the model's forecast reliability to deteriorate substantially. Analyses have shown that ARIMA-based forecast error expanded by 30% to over 40% compared to normal periods during events like the 2008 financial crisis and recent trade tariff shocks.

Additionally, because ARIMA is a univariate model that considers only past price data, it cannot incorporate external factors that directly influence prices—such as oil price movements or national tariff policies. In practice, forecast error grows noticeably once the prediction horizon extends beyond three months, a limitation frequently cited by practitioners.

Even before adopting statistical models, many raw materials procurement organizations still rely on tracking prices manually in Excel spreadsheets or making decisions based on experience. While this approach may not pose major issues when markets are stable, the picture changes dramatically when multiple macroeconomic indicators are moving simultaneously. Simply gathering and analyzing the necessary information takes considerable time, and decision-making speed inevitably falls behind the pace of market change.

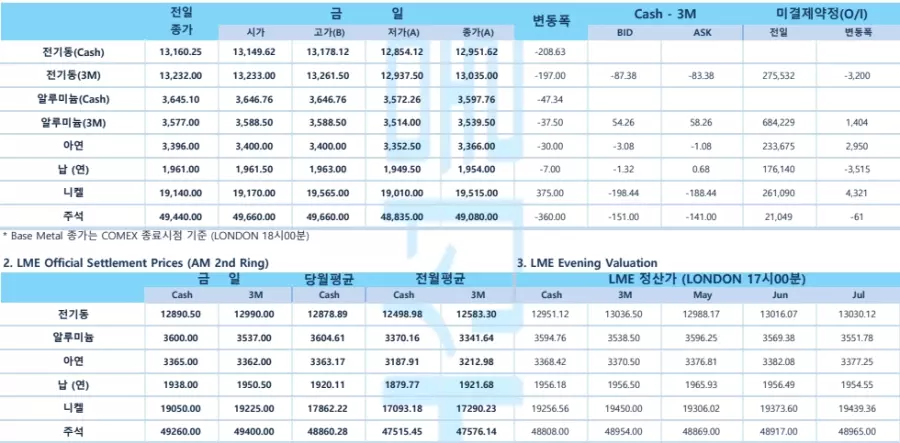

There is also a practical reality to contend with: final transaction prices for raw materials are frequently determined by reference to LME or CME closing prices. These closing prices are typically finalized after domestic business hours, when the London or U.S. markets close. As a result, procurement officers arrive at their desks each morning needing to first review the previous night's settlement prices, then scan the day's market news before they can begin making sourcing decisions. By the time they have gathered the information and prepared reports, the time available for actual strategy development has already shrunk considerably.

The fundamental reason raw material price forecasting in the steel and construction industries is so challenging is that individual commodity prices do not move independently—they are complexly intertwined with global macroeconomic variables. A prime example is the relationship between international crude oil prices and copper prices.

When international oil prices surged during the Strait of Hormuz crisis in March 2026, two opposing forces acted on the copper market simultaneously. On one hand, rising energy costs for mining, smelting, and ocean freight directly increased copper's production cost floor. On the other hand, the oil price spike burdened the real economy, dampening demand across the manufacturing sector.

According to J.P. Morgan Research, a 10% surge in international oil prices reduces global GDP growth by approximately 0.16 percentage points. Because copper demand is highly sensitive to GDP fluctuations, the cost-push effect from the supply side and the demand-destruction effect can either offset or amplify each other—creating a complex dynamic that defies simple directional predictions.

In a structure where a single macro event affects a single commodity through opposing pathways, linear reasoning such as "oil goes up, so copper goes up" is insufficient for predicting price direction.

Another critical variable affecting raw material prices is the U.S. Producer Price Index (PPI) and the monetary policy stance linked to it. According to the U.S. Bureau of Labor Statistics (BLS), the final demand PPI for May 2026 rose 1.1% month-over-month and surged 6.5% year-over-year. In particular, price increases in energy and basic chemical feedstocks at the intermediate goods stage are clearly transmitting through to downstream industries.

When this kind of price pressure persists, the probability of a Federal Reserve rate hike rises. Higher interest rates tend to strengthen the dollar, which in turn raises the effective purchase cost for companies procuring raw materials in non-dollar currencies. The backdrop to copper's pullback in Q2 2026 after reaching an all-time high earlier in the year included precisely this kind of rate-hike anxiety. Without examining the entire transmission chain—inflation → interest rates → exchange rates → raw material prices—it is difficult to accurately gauge the direction of any individual commodity.

To summarize: raw material prices in the steel and construction industries are determined by a confluence of fundamentally disparate variables—geopolitics, energy prices, trade policy, inflation indicators, and green transition demand. Tracking any single variable in isolation makes it impossible to see the full picture. What is needed is a tool capable of analyzing the compound impact that emerges when multiple variables shift simultaneously.

This is precisely why AI forecasting models are attracting particular attention in these industries. AI models do not look at historical prices alone. They learn from hundreds of distinct variables simultaneously—crude oil prices, PPI, dollar exchange rates, tariff rates, production quota regulations, energy consumption data, and more. Where legacy statistical models extrapolate the future from past price patterns, AI models assess the current state of the causal factors driving prices and form forward-looking judgments. The approach itself is fundamentally different.

Forecast accuracy in raw material price prediction depends more on the quality and diversity of input data than on model complexity. The data required to implement AI-powered price forecasting in the steel and construction industries can be organized into four domains.

The first is historical price data for the target commodities. Daily or weekly price data from international futures exchanges such as the LME and CME forms the foundation of time-series modeling, and long-term datasets spanning decades help identify cyclical patterns.

The second is macroeconomic and financial indicators. This includes international crude oil prices (Brent, WTI), U.S. PPI, GDP growth rates for major economies, benchmark interest rates, the U.S. Dollar Index (DXY), and major currency exchange rates. As discussed earlier, these indicators form complex correlations with raw material prices, so the forecasting model must be able to incorporate them in near-real time.

The third is supply-demand data. This encompasses production volumes from major producing countries (Australia, Brazil, Indonesia), import-export trade volumes, inventory levels, and commissioning timelines for major new supply sources such as Guinea's Simandou project. On the demand side, key variables include China's steel production output, global construction permit statistics, and data center construction pipelines.

The fourth is policy and geopolitical data. This includes tariff rate changes across countries (e.g., U.S. Section 232), production quota adjustments by producing nations (e.g., OPEC policy), shipping lane status for major maritime routes, and environmental regulation tightening trends. Because this data domain encompasses not only quantitative figures but also unstructured information such as news and policy announcements, the AI system's ability to analyze text data and assess market impact is also critical.

As raw material price volatility intensifies, interest in AI-powered forecasting systems is expanding rapidly. According to a 2025 survey by ABI Research, 94% of global supply chain professionals plan to deploy AI in decision-support functions within the next 24 months. Gartner projects that 70% of large global enterprises will adopt AI-powered demand and cost forecasting as a core supply chain engine by 2030. That said, only approximately 23% of companies currently have a formal AI roadmap in place, indicating that a gap remains before widespread adoption reaches full scale.

According to McKinsey's analysis, companies that proactively adopted AI-powered forecasting systems are realizing operational cost reductions of 15% to 25% compared to competitors, and forecast error rates have been reduced by 20% to 50%. These improvements in forecast precision translate directly into reduced safety stock buffers and significantly lower opportunity costs from stockouts.

The steel industry is among the sectors where AI-powered procurement forecasting has been most actively applied. According to a C3 AI case analysis, a global steel manufacturer with over $35 billion in annual revenue deployed an AI-powered demand forecasting and raw material optimization system. The result was forecast accuracy reaching as high as 98% in certain raw material segments and a net 1% reduction in total raw material purchasing costs, yielding approximately $42 million in annual cost savings.

India's Tata Steel established a global Intelligent Remote Operations Centre (iROC) to centrally manage decision-making across five major steel plants nationwide, equipping it with a digital brain system comprising over 260 AI algorithms. This reportedly enabled a proactive sourcing framework that pre-adjusts procurement pricing upon detecting geopolitical signals and flexibly shifts contract timing accordingly.

Beyond steel, Walmart refined its cost and demand forecast accuracy by 1.7% through AI algorithms, driving billions of dollars in annual cost efficiencies. Nestlé reduced forecast error across its raw material supply chain by more than 40% following the deployment of AI models.

Developed by ImpactiveAI, Deepflow Materials is an AI solution that integrates price forecasting, market analysis, technical analysis, and an AI assistant within a single platform—connecting the entire workflow from prediction to judgment in one seamless flow. Built on over 224 deep learning and machine learning models and 72 AI patents, it delivers short- and medium-term price forecasts for core commodities—including steel, non-ferrous metals, energy, and agricultural products—via an interactive dashboard. The range of forecast-covered items continues to expand based on client requirements.

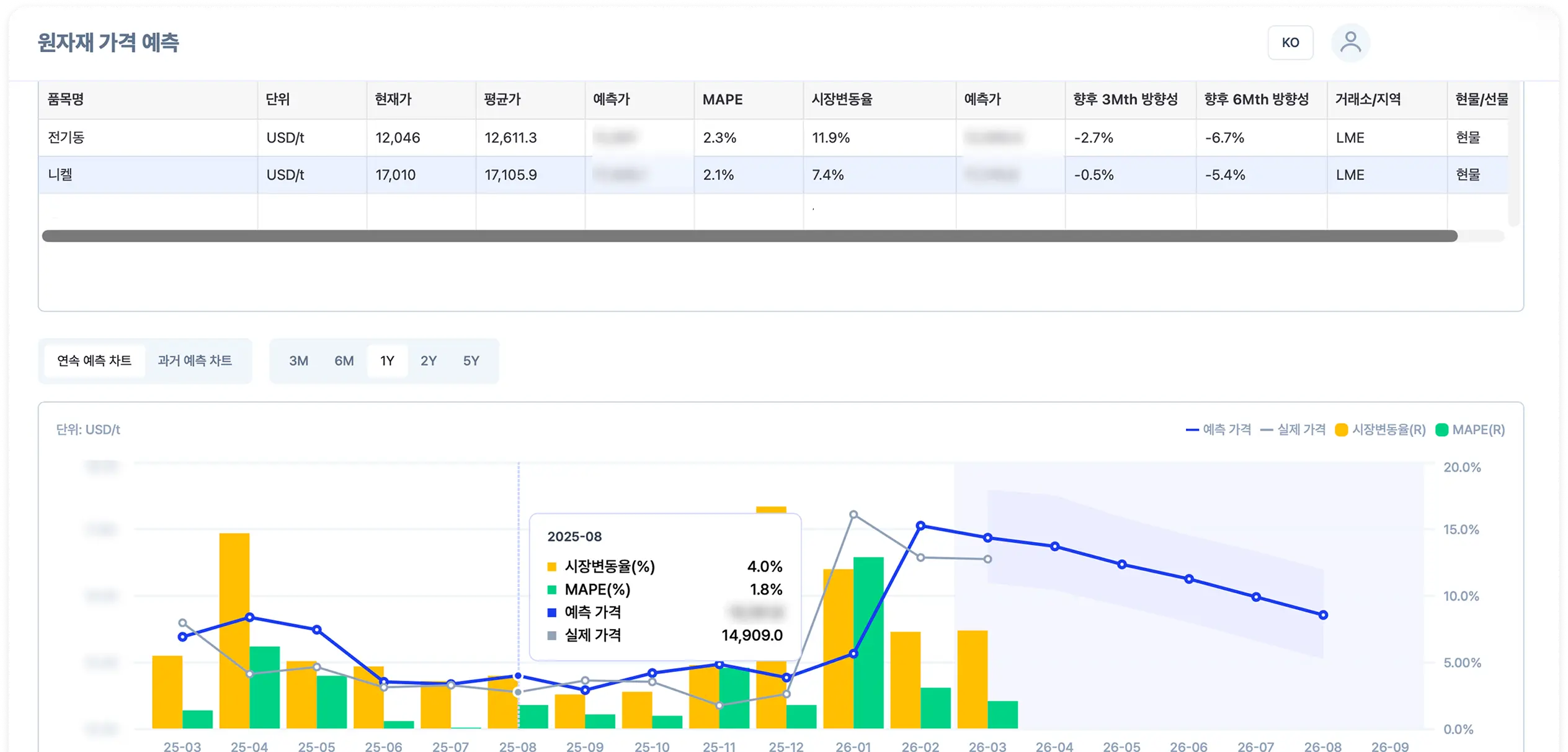

Deepflow Materials generates forecasts by jointly learning from diverse variables that influence prices—including production, consumption, and trade data, economic indicators, key events, and climate factors. Because it provides both 6-month long-term forecasts and 5-week short-term forecasts simultaneously, strategic decisions such as annual fixed-price contracts and tactical responses such as weekly spot purchases can both be evaluated on a single screen.

For example, if a copper procurement manager is approaching a quarterly contract renewal, they might first check the long-term track for the medium-term directional outlook and then use the short-term track to decide whether to accelerate the contract timing.

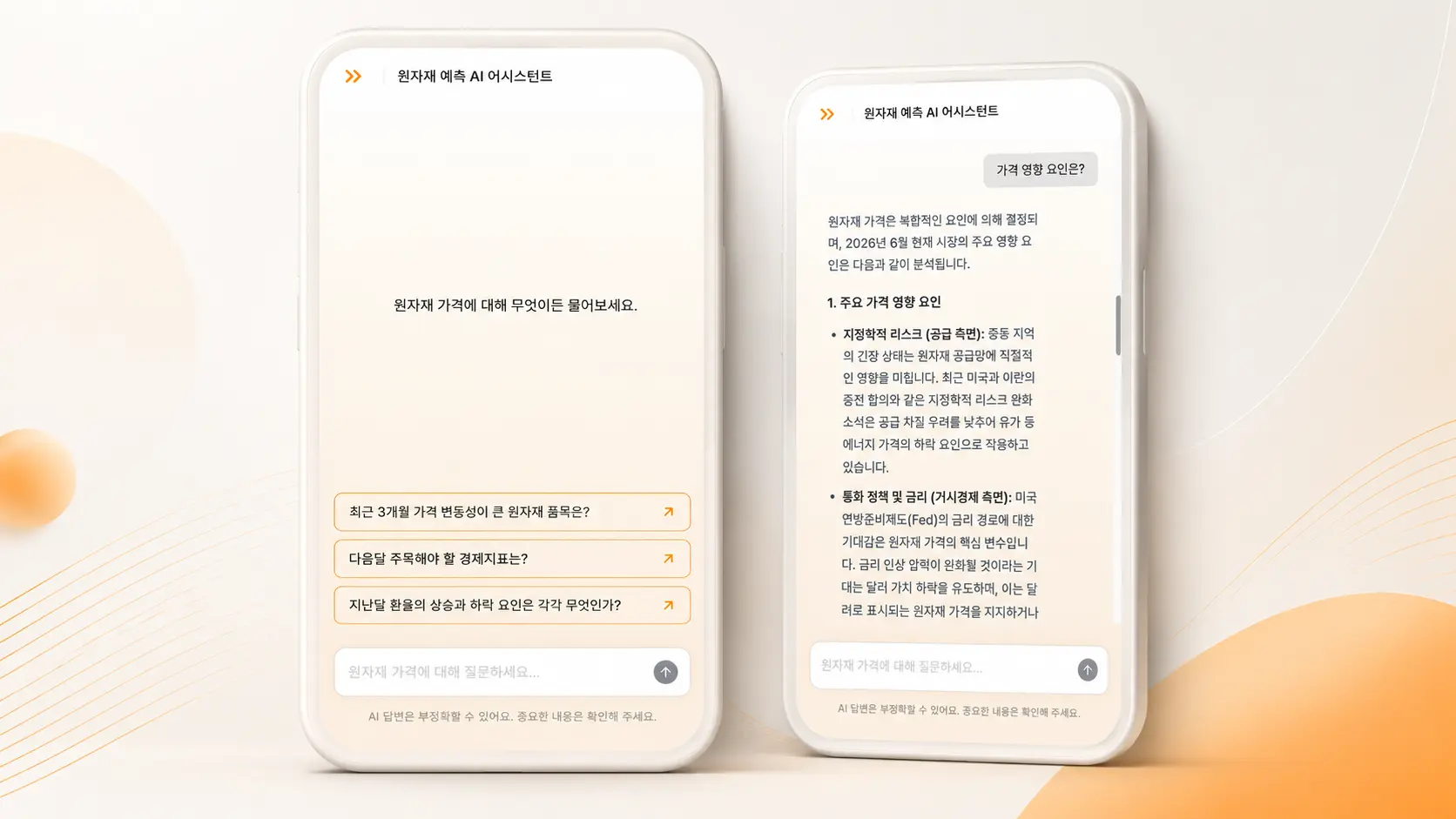

The AI monitors global news around the clock, identifying the key factors—such as exchange rate shifts or supply chain disruptions—that drove price movements and quantifying their impact. Because it also presents the correlations and causal relationships between factors, procurement teams can understand why prices moved on a data-driven basis.

As discussed earlier, commodity settlement prices are finalized after domestic business hours. With Deepflow Materials, the AI compiles its overnight market analysis so that procurement officers can review it immediately upon arriving at their desks and move straight into decision-making and reporting.

The system predicts the price direction for the coming week on a five-level scale from strong rise to strong decline, accompanied by probability values for each scenario. Four indicators—direction, volatility, trend strength, and trend persistence—are displayed as scores, providing an at-a-glance read on market conditions.

For instance, if the probability of a "moderate decline" is highest at 62% and trend persistence is also high, that provides a data-backed rationale for deferring a purchase by one week. If the probability of a "strong rise" is high, the case tilts toward preemptive buying.

Users can ask questions in natural language, and the assistant synthesizes forecast results and market data to deliver concise summaries. Ask "Summarize next month's nickel price outlook and the key drivers," and the AI assistant instantly generates a briefing that includes the forecast value, primary influencing factors, and market context. Procurement officers can use this as a starting framework for reports, significantly reducing the time spent on information gathering and interpretation.

In a real-world deployment, domestic construction company B adopted Deepflow Materials to reduce uncertainty in raw material procurement decision-making. The company ran price forecasts on four commodities—rebar, copper cathode, hot-rolled coil, and thermal coal—over an approximately seven-week period. The result was an average forecast accuracy exceeding 96.6% across all commodities, with a peak of 98.5%. Company B confirmed the potential to apply these forecasts to purchase timing decisions, order priority adjustments, and long-term contract simulations, and is now pursuing a transition from experience-based judgment to a data-driven decision-making framework.

Before adopting an AI price forecasting system, three core areas should be assessed.

The first is data readiness. Because forecast accuracy depends on data quality, organizations should verify that internal data—such as historical purchase records and inventory status—is consistently organized and maintained. External data is often collected automatically by the solution, so focusing on internal data management tends to yield the greatest returns.

The second is workflow integration. For AI forecasts to translate into actual procurement actions, the system needs to be designed to integrate naturally into existing workflows—including ERP connectivity and approval processes.

The third is establishing performance benchmarks. Pre-implementation metrics such as forecast error rates, inventory turnover ratios, and unit purchase costs should be documented in advance so that post-implementation improvements can be measured objectively.

Q. What is the most significant difference between AI and legacy statistical models for raw material price forecasting?

Legacy statistical models estimate the future based on patterns in historical prices. AI models, by contrast, analyze external variables that drive prices—including crude oil prices, exchange rates, tariffs, and production quotas—alongside historical data to produce forecasts.

Q. Does implementing an AI forecasting system require changes to existing ERP systems or business processes?

No separate system changes are required. Forecast outputs can be used immediately as a reference input within your current procurement decision-making process.

Q. Can the system forecast commodities for which data is limited?

Deepflow Materials operates its own forecasting models based on publicly available market prices and macroeconomic indicators, so most commodity items can be forecasted without requiring client-side data. Forecast values are already available for a wide range of commodities, allowing users to begin immediately after subscribing—with no separate data preparation process required.

The global raw materials market volatility that has persisted since 2025 is not a temporary phenomenon. It is more accurately understood as the beginning of a new market environment shaped by geopolitical realignment and the energy transition. To build competitive procurement strategies in this environment, organizations need tools that can analyze the multiple variables driving prices in real time and respond proactively.

Deepflow Materials is an AI solution designed to help raw materials procurement professionals in the steel and construction industries make more accurate, data-driven purchase timing decisions and execute strategic sourcing. If you would like to see how the platform works and review actual forecast results firsthand, apply for a two-week free demo trial.

.svg)

.svg)