.svg)

.svg)

Download Brouchure

%202.svg)

Oops! Something went wrong while submitting the form.

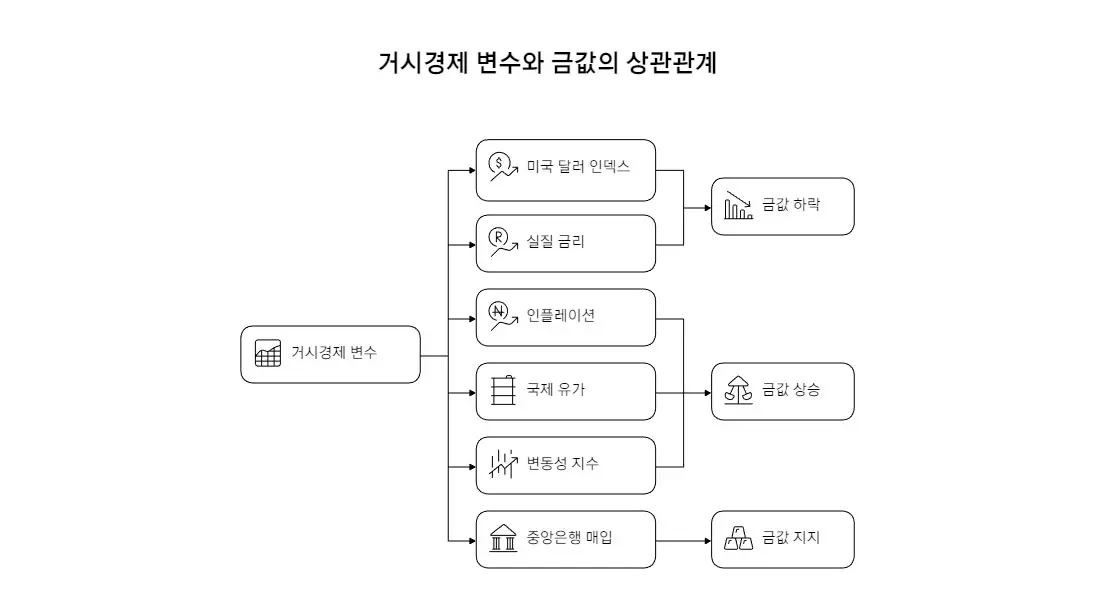

Gold is traded in U.S. dollars on global markets. When the dollar strengthens, gold becomes more expensive for holders of other currencies, dampening demand. Conversely, a weaker dollar makes gold more attractive, driving prices up. Econometric analysis shows that a shock to the Dollar Index tends to suppress gold prices sharply for roughly three periods before the effect gradually fades.

Gold is a non-yielding asset — it pays no interest. When real interest rates rise, capital flows toward yield-bearing instruments like deposits and bonds, putting downward pressure on gold. When real rates drop or turn negative, the opportunity cost of holding gold shrinks, making it more likely to appreciate. This is precisely why gold prices react so sensitively every time the Federal Reserve announces a rate decision.

When inflation starts to climb, investors seek out physical assets like gold as a hedge against currency devaluation. Over the long run, gold prices tend to keep pace with — or outpace — inflation, a pattern that becomes especially pronounced during periods of economic stress.

Crude oil prices are also closely linked to gold. Oil is not only a major driver of inflation but also determines the energy costs of mining gold. Gold extraction requires massive amounts of electricity and fuel, and transportation costs are directly tied to oil prices — so when crude rises, gold production costs follow. In practice, oil is consistently cited as one of the most significant variables in gold price forecasting models.

When uncertainty and fear grip the market, investors tend to flock to gold as a risk-off play. The VIX — the market's so-called "fear gauge" — captures this dynamic. When equity markets sell off sharply or geopolitical crises escalate, the VIX spikes, and gold prices often follow. Interestingly, even when other economic indicators lose their explanatory power, the VIX maintains a consistently positive correlation with gold. This underscores gold's dual role as both an economic asset and a psychological safe harbor.

While macroeconomic variables explain short-term price swings, long-term price direction is ultimately shaped by supply and demand fundamentals. The most notable shift in the gold market recently has been the strategic gold accumulation by central banks worldwide.

Following the financial sanctions imposed on Russia in 2022, emerging-market central banks began diversifying away from dollar-denominated reserves — resulting in a record 1,136 tonnes of gold purchases that year alone. Gold demand is price-elastic on the buy side but supply is notably inelastic. This type of demand tends to persist even as prices rise, effectively creating a strong price floor.

Add to this the robust jewelry demand from Asia — particularly India — and the steady industrial demand driven by AI semiconductors and other applications, and gold has a structural support base that makes it resistant to falling below certain levels.

Efforts to forecast gold prices began with econometric models that statistically analyzed historical price data, then progressed through machine learning and into today's highly sophisticated deep learning architectures. This section traces how each technology works, where its limitations lie, and how the next generation of models overcame them.

The Autoregressive Integrated Moving Average — ARIMA — is the oldest and most widely used method in financial time-series forecasting. Think of it as using recent price trends and error patterns to estimate tomorrow's price. It combines past values (AR) and past forecast errors (MA) to model time-series data, applying differencing to remove non-stationarity.

Empirical studies have shown that ARIMA(2,1,2) and ARIMA(4,1,4) models deliver reasonably strong short-term accuracy for gold prices, with R² values around 0.85–0.90. The model's transparent, interpretable mathematical structure is another key advantage.

Financial data frequently exhibits volatility clustering — periods of high volatility tend to beget more volatility, while calm periods persist. The GARCH model was built specifically to capture this behavior.

Hybrid ARIMA-GARCH approaches can forecast not just the mean trajectory of prices but also the variance dynamics. This combined approach has consistently outperformed standalone ARIMA in the notoriously volatile gold market. That said, these classical models are fundamentally grounded in linear assumptions, which creates structural limitations when trying to predict the sharp, nonlinear movements gold is known for. This is where machine learning enters the picture.

Where traditional statistical models focus on linear relationships, machine learning models can uncover complex, nonlinear structures hidden in high-dimensional data.

Random Forest builds multiple decision trees independently and aggregates their outputs to produce a final prediction — similar to polling a panel of experts and synthesizing their views. This approach effectively controls overfitting and remains robust even in the presence of outliers. In practice, Random Forest has achieved R² values exceeding 97%, significantly outperforming traditional regression.

Gradient boosting methods (XGBoost, LightGBM, etc.) learn iteratively, with each successive model correcting the errors of its predecessor, resulting in substantial accuracy gains. One of their major advantages is feature importance ranking — identifying which variables drive gold prices the most. Recent SHAP analyses have revealed that the Dollar Index and oil prices explain over 70% of gold price variation.

Machine learning performance ultimately comes down to the quality of inputs. State-of-the-art gold forecasting models go far beyond raw historical prices. They incorporate 20-day, 50-day, and 200-day moving averages to capture both short- and long-term trends, momentum indicators like RSI and MACD to identify overbought and oversold conditions, and Fibonacci retracement levels to pinpoint support and resistance zones. Combining these diverse features is what allows ML models to forecast gold prices with far greater precision.

If machine learning demonstrated the ability to handle nonlinearity, deep learning added the dimension of learning across time. Financial data is inherently sequential — past trends continuously influence present outcomes. Standard RNNs can track temporal patterns to some extent, but they suffer from the vanishing gradient problem: as sequences get longer, earlier information fades away.

LSTM was designed to solve this. Its forget gate discards irrelevant information, its input gate selectively retains what matters, and its output gate produces the final prediction. The result is a network that preserves critical long-range dependencies while filtering out noise.

In gold price forecasting experiments, LSTM has achieved accuracy of approximately 97.68%, effectively capturing long-horizon market dynamics. GRU — a streamlined variant of LSTM — uses only two gates, reducing computational overhead while delivering comparable performance. This makes GRU particularly useful for tracking gold price movements in resource-constrained environments.

Originally developed for image recognition, CNNs can also be applied to one-dimensional time-series data to extract localized patterns — detecting short-term price spikes or dips the way an image model identifies visual features.

Hybrid models combining CNN with LSTM or GRU learn both complex spatial features and temporal dynamics in a single pass. Research shows this approach delivers 22–48% performance improvements over standalone models. The CNN-GRU variant, in particular, has achieved R² values of 0.98–0.99 with an MAE of 9.46.

The Transformer architecture that revolutionized NLP is now making its mark in time-series forecasting. Its core innovation — the self-attention mechanism — allows every time step in the data to reference every other time step, extracting the most relevant information for the current prediction. Unlike RNNs, which process data sequentially, Transformers attend to all time steps simultaneously, ensuring that distant information is never lost.

Applied to gold price forecasting, Transformer-based models have achieved R² values of 0.988–0.993. When referencing lookback windows of 15 days or more, they converge far more reliably than CNN or LSTM architectures. The trade-offs include the mandatory positional encoding to preserve sequence order and quadratically increasing computational costs as input length grows.

Several specialized Transformer variants have emerged to address vanilla Transformer's computational constraints. Informer introduces ProbSparse attention — selecting only the most informative queries — to reduce complexity to O(L log L). Autoformer embeds time-series decomposition within the Transformer architecture, enabling the model to learn seasonal and trend components separately. Reformer leverages locality-sensitive hashing to improve computational efficiency.

Research results show that Informer effectively filters short-term noise while better capturing long-range gold price trends, reducing forecast error by approximately 10–25% compared to RNN-based models.

Gold prices don't move on quantitative data alone. Unstructured text — news articles, social media, analyst reports — carries market sentiment that can significantly influence prices. When headlines report a stock market crash or escalating geopolitical tensions, gold demand often reacts before any hard economic indicator shifts.

To quantify this phenomenon, NLP techniques are now widely used in gold price forecasting. FinBERT — a language model fine-tuned for financial text — can extract positive, negative, and neutral sentiment from news headlines. Research has confirmed that higher sentiment scores correlate with rising gold prices, and that incorporating these scores into existing forecasting models meaningfully improves accuracy.

Large language models like GPT-4 are also being used to parse the nuances of complex geopolitical news and gauge market direction. That said, for real-time price prediction, FinBERT-LSTM hybrid approaches currently deliver stronger results. As LLM capabilities advance, research integrating quantitative and qualitative analysis into a unified framework is expected to accelerate.

Recent research increasingly centers on hybrid systems that combine the strengths of different models — typically using preprocessing or post-calibration stages to compensate for single-model limitations.

Raw gold price data is inherently noisy. Decomposing it into multiple frequency components and training models on each component separately has proven highly effective. Empirical Mode Decomposition (EMD) breaks time-series data into Intrinsic Mode Functions (IMFs), enabling models to learn distinct characteristics independently.

The EMD-LSTM approach — which separates price data into trend and residual components before feeding them into LSTM — is a prime example of this technique significantly boosting forecast accuracy. Wavelet analysis examines data in both time and frequency domains, removes noise, and then feeds the cleaned signal into neural network models.

Gold prices contain multiple overlapping cycles — daily, weekly, monthly, and multi-year — all superimposed. Recently developed CNN-GRU models employ a "multi-cycle forecasting framework" that learns across these different time horizons simultaneously, delivering approximately 22% or greater performance gains over conventional approaches.

Transfer learning — pre-training models on equity or other commodity market data before applying them to gold — is another active research area. This method can capture complex patterns that gold data alone might miss by leveraging insights from related markets.

Despite cutting-edge technologies being brought to bear, significant challenges remain.

The Efficient Market Hypothesis holds that all available information is rapidly priced in, making it inherently difficult to generate alpha from historical data alone. Deep learning models are susceptible to overfitting — learning noise rather than signal — making rigorous out-of-sample validation essential.

AI models are often characterized as "black boxes," where the reasoning behind predictions can be difficult to articulate. Explainable AI techniques like SHAP analysis and attention map visualization are being deployed to address this, playing a critical role in building the trust decision-makers need to act on model outputs. Developing robust methodologies for responding to "black swan" events — wars, pandemics, and other unforeseen disruptions — remains an ongoing challenge.

On the practical front, securing clean and sufficient data, provisioning the compute resources needed for model development and production, and building the organizational capability to translate forecast outputs into actionable business decisions are all equally critical. As models grow more sophisticated, the demand for expertise in data preprocessing and feature engineering rises in tandem. Success hinges not just on deploying a model, but on designing end-to-end processes that ensure forecast insights are effectively operationalized across the organization.

Forecasting commodity prices is far more complex than it might appear, and building all the requisite capabilities in-house is a tall order for most organizations. Predicting gold alone requires simultaneously managing macroeconomic variable integration, nonlinear model design, and much more.

ImpactiveAI's Deepflow — an AI-powered demand and price forecasting platform — addresses this complexity through a unified solution.

For commodities like gold, where nonlinearity and volatility are extreme, no single model can capture every movement. Traditional time-series models perform well in stable regimes, while deep learning models excel during periods of rapid change.

Deepflow maintains a library of over 200 deep learning and machine learning models and automatically selects the optimal model combination based on the characteristics of the target data. This represents a practical, production-grade implementation of ensemble learning and hybrid modeling principles. The 72 patents underpinning this capability include model selection algorithms specifically designed for materials demand forecasting patterns.

Gold price forecasting technology has evolved from simply tracking historical prices to automatically analyzing complex macroeconomic dynamics and quantifying market sentiment. As outlined throughout this article, the convergence of three pillars — thoughtful macroeconomic variable integration, advanced nonlinear modeling, and NLP-powered sentiment analysis — forms the foundation of high-precision forecasting.

Going forward, the field won't stop at improving accuracy. Explainable AI (XAI) will be leveraged to make forecast rationale transparent and specific, and alternative data fusion will be used to infer patterns like undisclosed central bank gold accumulation. Gold isn't just another commodity — it's a barometer of the global economy. That's why the pursuit of more precise gold price forecasting will remain a defining challenge in modern financial engineering.

.svg)

.svg)